To help your clients with Disability Insurance, what should you know?

Value quality over price.

Expect to pay 1 to 4 precent of your income for a good individual disability insurance policy. With some purchases, cheaper is not necessarily better. Three things that come to mind are life preservers, heart surgery, and disability insurance.

Disability insurance is not a commodity; it is a contract that clearly spells out when a claim will and will not be paid. There are significant differences between plans beyond the price. Before suggesting buying anything, make sure you clearly understand the contract.

Look at the company ratings.

A disability company you recommend could potentially pay your client’s salary for the next 20 years. It is important they be financially sound. All disability companies are rated by third party companies. ProducersXL do not recommend anything lower than an “A” rating.

Make sure you understand the definition of disability.

It is preferrable to invest in a policy that pays a benefit if unable to work in your current occupation versus one that pays only if unable to work in any occupation.

Consider the inflation protection benefit.

A person disabled for 20 years with a $5000 per month benefit would be paid a cumulative benefit of $1,200,000 without adjusting for inflation; if increased by 3 percent per year to adjust for inflation, the cumulative benefit would be $1,641,000.

The 90-day waiting period is usually the most cost effective.

A policy with a 90-day waiting period will cost substantially less then one with a 30-day or 60-day period. Increasing the period beyond 90-days does not reduce the premium by much.

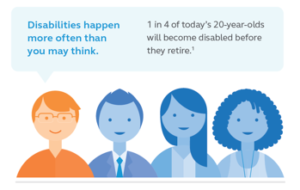

As a professional, you play an important role in helping clients understand the risks to their financial security and providing clients the protection they need. Clients are aware why they need to purchase Life Insurance, but are they aware of protecting their finances while they are still here? Most people have never been approached about disability insurance and don’t know they need it. Whether you’re talking to individuals, business owners or their employees, it’s important to establish the need for coverage. Your job is to help them along the path to purchase—from awareness to buying.

Key success factors:

- Hone your presentation style. Develop a conversation plan. Explain the benefits of the policy, not just the product features or riders. Keep it simple.

- Provide options. Showing different price points gives clients the power to choose.

- Share real life stories. If you don’t have a personal story, ask me for some real-life testimonials that illustrate how having disability insurance can make a big difference in people’s lives.

- Share the promise being made. Your clients are purchasing a promise that they will have income protection when they experience the unexpected.

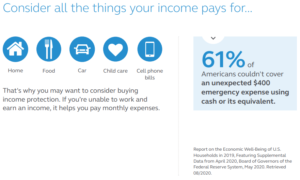

Reach out to me for any help in developing a plan to help your clients find the income protection that best fits their needs.

For more Industry News and Tips and Resources regarding Disability Insurance,

Reach out to Kristi Brin.